In the side streets of old Dehli a gold shop sells bangles, baby jewellery, bullion and coins. All yellow 22 and 24 carat gold. Its shopkeeper changes his prices daily, using the London price fix as his benchmark and charging a small premium to help his profits.

Meanwhile in mainland China, the Shanghai Gold Exchange (SGE) oversees gold imports, most notably via Hong Kong. It is the largest physical gold market in the world yet like the small Indian gold shop, the SGE relies on the previous day’s London price fix as its pricing benchmark.

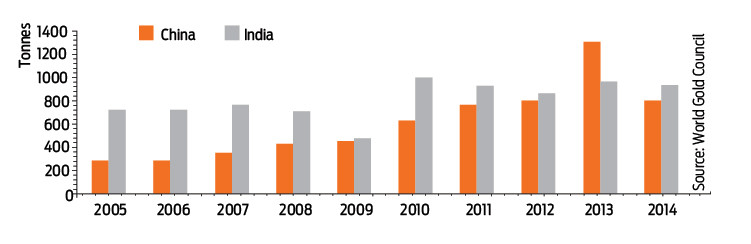

Asian dominance

Between them, India and China dominate global physical gold demand. In 2014 the World Gold Council (WGC) estimates approximately 3,900 tonnes of global physical demand of which circa 800 tonnes goes to China and 800 tonnes to India. Chinese gold consumption is more than 800 tonnes, in fact much much more. In November 2014, Xu Luode the Chairman of the SGE told a conference that China would import 1,200 to 1,300 tonnes in 2014. The WGC needs to step up its game.

(Click on chart to enlarge)

What matters is that the Chinese and Indians are the powerhouses of the gold market. Yet perversely both countries, and indeed the whole world, is beholden to a gold price 'fixed' in London and influenced by round the clock futures trading on the COMEX platform in the US.

Price formation is the subject of heated discussion amongst participants and commentators on the gold market. Some believe the market is manipulated, that Western governments, big banks and to some extent speculators, collude to keep the gold price down, thereby protecting the US dollar’s and other currencies’ value.

Certainly, the gold price is relatively easy to manipulate. The futures market can be used to take long and short bets which can then be settled with no physical gold changing hands. For example you could sell large quantities of gold futures over a short period to shock the market and then buy back your position in a more measured way to limit upward price pressure. The disparity between the huge value of gold contracts traded at COMEX and the small value of the bars (good for delivery) in its warehouse demonstrates the synthetic nature of that market place.

So why do the Chinese and Indians accept this state of affairs, where Western markets set the price? After all, they buy most of the newly produced gold yet have almost no say in price formation. The answer is that it suits them, at least for now. The current gold price is only 20% higher than the average cost of production and at some major gold mines production cost equals the current gold price. So the Chinese are thinking 'if you want to sell me gold for little or no profit then you are very welcome'.

Not only does China and India buy newly mined gold, they are also buying gold from Western investors. Over the last two years privately owned Western gold stocks have been rapidly depleting while Asian stocks increase steadily, leading to the simple conclusion that gold is moving eastwards.

Drawing conclusions

What does this mean for investors? Should we be buying physical gold, gold ETFs or gold equities? These are difficult questions to answer, especially while the market is so volatile and potentially subject to manipulation. Some people argue that gold should be seen as an insurance product not an investment, that you should buy a small quantity of physical on a regular basis irrespective of the prevailing price.

I think the most important takeaway is not to dismiss the importance of gold to the Chinese, Indians and many other countries and regions (for example Russia, Turkey, Brazil, Middle East) all of which are net buyers and regard gold as the safest type of money. Also don’t imagine that Western central banks don’t have the utmost respect for gold. In recent years both the German and Dutch governments have moved to repatriate their gold reserves, probably because they fear the custodian (in the former’s case the US Federal Reserve) might lend or even sell their gold to someone else.

In terms of the gold price, although very hard to forecast, there could come a time when Asian and other non-Western demand outstrips physical supply. Recent data shows that UK, Swiss and even Hong Kong vaults are very low of stock. Supply from the mines and gold recyclers has evidently been insufficient to satiate Asian demand.

When stocks in Western gold vaults are too low to satisfy that additional Asian demand, the influence of the COMEX futures and London price fix could wane. Interestingly, in recent weeks the Shanghai Gold Exchange has made moves to create an international physical gold market which could easily become the leading market, and where gold prices are formed in the future. This would transform the industry, should reduce gold price volatility and would be good news for gold miners and gold investors alike.

Charles Long resources analyst at Sanlam Securities