Magazines-to-education supplies distributor Smiths News (NWS) illustrates how a business can grow profits without a major increase in revenue. While growing the top line is essential for longer-term gains, today's results from Smiths illustrate the power of cost cutting and rebalancing group activities towards higher-margin activities.

Group revenue increased by 0.4% to £1.8 billion. Underlying pre-tax profit increased by 11.6% to £53 million. Net debt is down 2% to £98.5 million. The dividend is up 8.1% to 9.3p.

The market is clearly pleased with the performance as the shares rise 8.3% to 210p. That means the stock has risen 175% since the start of 2012, a re-rating driven by expansion into the schools market and modernising its books business. The issue to consider is that cost cutting can't go on forever, so Smiths cannot ignore the pedestrian top line.

The stock was previously marked down as investors worried about its core magazines and newspapers arm being in terminal decline. That continues to throw off lots of cash and has excellent earnings visibility due to long-term contracts, yet the key point for investors is that Smiths News is becoming less dependent on this operation.

The £384 million cap now derives 29% of group profits outside of newspaper and magazine wholesaling, up from 27% six months ago. It is targeting 50% of profits from outside this segment by 2016.

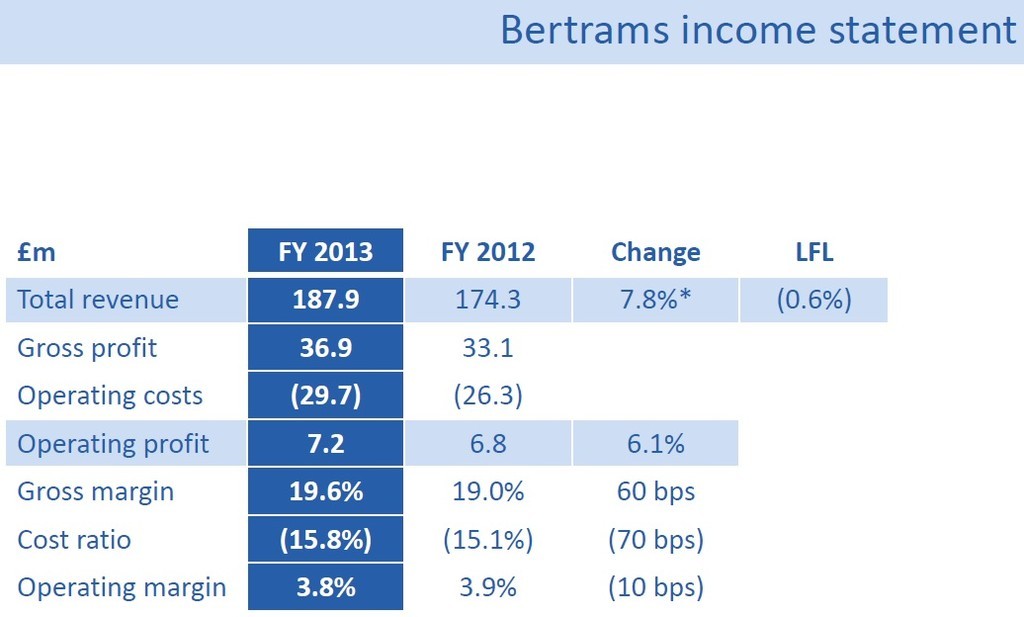

Bertrams, which is the book wholesaler, is doing particularly well with growth in internet, international and academic e-book sales. Last November it launched a direct-to-consumer brand called Wordery. To date it has sold more than 1 million books through online marketplace sites like those offered by Amazon. Wordery's own website launched a few weeks ago. Chief executive officer Mark Cashmore says sales through this channel should get higher profit margins as there's no commission to be paid like the marketplace sites.

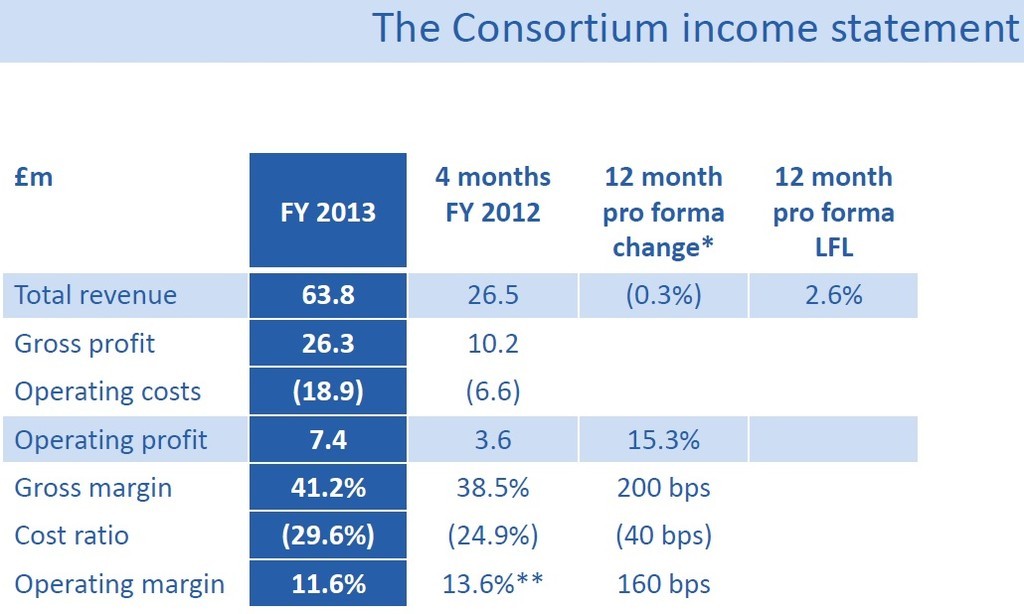

The education, care and early years supplies business, called Consortium, looks disappointing from a revenue perspective. On a like-for-like basis, sales were only up 2.6%. Cashmore claims there's been a shift in school buying patterns. He says April, July and September have historically been peak periods for demand. 'The buying patterns are now levelling off as more schools convert to academy status.' He says 6.4% like-for-like education sales growth over the peak period is more indicative of what the division should achieve in the future. 'We're not chasing sales at the expense of margins,' insists the CEO.

House broker Liberum Capital upgrades its price target from 203p to 220p. It forecasts 21.4p earnings per share for the year to August 2014. That puts the stock on a price to earnings ratio of 9.8 times. A forecast 9.7p dividend per share equates to a prospective 4.6% dividend yield. That's still an attractive income but you could argue the stock looks fair value. We'd want to see the education arm step up a gear and potentially expand into another business line, applying its existing skills, as necessary fuel to sustain share price momentum.