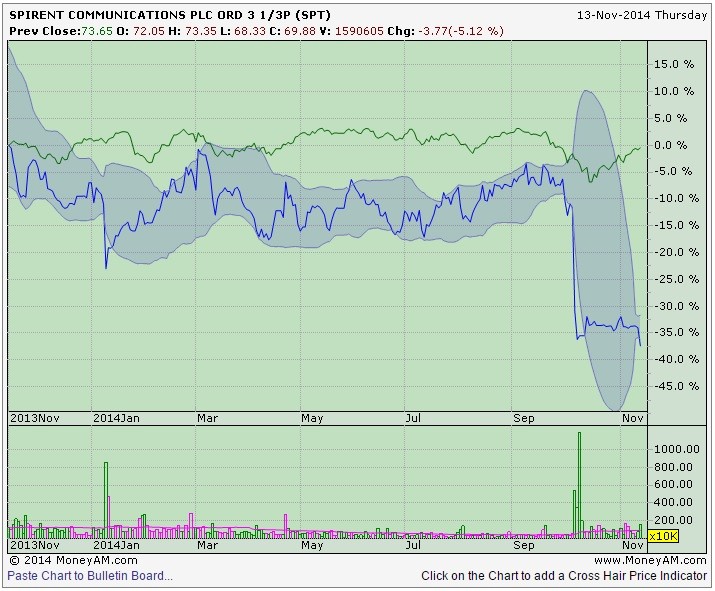

Today's third quarter trading update from testing kit supplier Spirent (SPT) offers plenty of food for thought. Revenues for the three months from though to September of $110.1 million is a fraction better than guidance of 'slightly below $110 million' issued in last months warning. The major weakness is on the Networks and Applications side of the business, worth 47% of first half revenues, or £104 million worth. Here revenues tot-up to $54.5 million, 7% off last year's equivalent $58.9 million that saw divisional operating profit collapse to just $1.1 million having run-up $8.2 million a year earlier.

In truth, there's a real hotch-potch of good and bad. On the negative side, where the market is clearly concentrating given today's 4.5% share price slump to 70.3p, there's a poor book-to-bill ratio in Networks of 91%, comments about trimming the cost base and a poor short term outlook not helped by a capex freeze at major customer AT&T (T:NYSE) as it mulls its own strategic shift to software defined network architecture, or SDN as it's known in acronym-land.

This is important because SDN (which allows networks to be controlled with lower level functionality) is where much of Spirent's R&D has been spent this year. Network Functions Virtualisation (NFV), is the other key R&D investment, which uses hybrid IT systems to connect networks.

Yet this points to the positives too. The wider telecoms industry is embracing new technology developments such as SDN and NFV which acts as a proof point of Spirent's strategic direction. IN other words, write more software into the kit. Holding revenue guidance for the fourth quarter (roughly $116 million anticipated) is a plus. And news that this is a grind it out market is not really news at all.

'Our jib is cut for improving conditions, so we remain on a broadly optimistic tack,' says Panmure's George O'Connor today.

'We believe it is clear that Spirent should be able to capitalise on its strong market position in comms test to return to historic levels of profitability in due course,' chime in Numis analsyts.

In the longer-term the shift into a more virtualised environment should mean a larger proportion of software revenues as the ‘virtualised’ software can run on cheaper and standard hardware, boosting profitability and, perhaps, visibility. But that transition is likely to take years, not months, and could open the door to new competitors entering the market. As Canaccord analyst point out today, 'there are already signs that open-source based testing solutions are gaining a foothold in the virtualisation testing market.'

The question facing investors right now is what are the catalysts that are likely to put some oomph into the share price, and in the near-term, the answer is, not a lot. Given Spirent's patchy track record, limited visibility, inherent cyclicality and absence of catalysts, there appears to be little reason for investors to pick up the phone to their broker anytime soon.