As we never tire of reminding investors, share certificates are not lottery tickets. They represent ownership of a stake in a company, its operating assets and ultimately its cashflow, not just lights that flash green and red as the share price jumps up and down on a dealing screen. This means you must do your research to ensure a firm is managed in your interests and has a strong competitive position and a value proposition. Otherwise, it may not be able to generate cash and if it does the board may do something silly with it.

Once a company is churning out this liquidity, management must first pay the bills - salaries, rent, rates, tax and interest on any debt. Failure to keep up with the last two in particular could prove terminal and leave shareholders with worthless paper, since other creditors get their slice of what is left long before those who own the equity in the event of a plunge into administration.

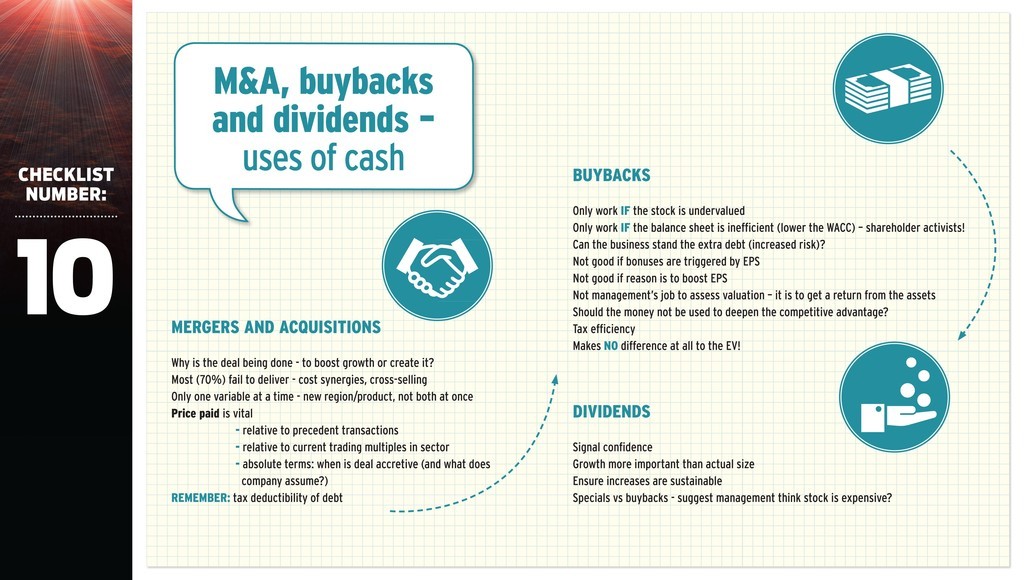

Once those hurdles are safely negotiated, a board has then several options available to it and a key skill of the best managers is an ability to allocate capital to the best effect, namely where it creates sustainable value for shareholders. They can:

? invest in the business to deepen its competitive advantage and sustain or improve the quality of earnings

? pay down debt to reduce risk

? make an acquisition to boost growth

? buy back shares and cancel them

? pay a regular or special dividend to shareholders

As this whole series makes clear, the first point is vital as without that the company is likely to go out of business quickly or at least be a rank bad investment. We are always happy to see the second, as debt is a killer, since the interest payments suck away valuable cash. The real controversy starts with the third, fourth and fifth points and which one brings the greatest benefit to shareholders. You must assess a company?s stated strategy here and check out its track record to ensure its suitability for your investment goals, time horizon, target returns and appetite for risk.

There is no ?right? answer but Shares is a huge believer in the power of dividends and how their reinvestment helps compound returns.

(Click on image to enlarge)

Done deals

Acquisitions are generally fraught with danger and should be approached with circumspection at all times. Royal Bank of Scotland (RBS) and Marconi are just two egregious examples of share prices laid waste by what the Financial Times? Philip Coggan once called ?the urge to merge? and too often deals are done for reasons of ego rather than business. Most fail to deliver the promised synergies, especially those which target increased revenues through cross-selling, and often management teams take on so much with integrating the new business they neglect the established one.

When it comes to deals, only back those which are designed to complement momentum and supplement a competitive position, not create them. Halma (HLMA) and Bunzl (BNZL) show how to do deals well, while Zattikka?s collapse into administration after the purchase of three operations at once to create a business for itself is a textbook example of how not to.

Price must be right

Share buybacks are equally controversial but they do have their place. If you do not sell any of your holding, then your percentage stake in the company?s equity increases. This is a good thing if you believe in the management and its competitive position as you now have a claim on a greater portion of future cashflow.

Buybacks can also be helpful if the net result is a conclusive reduction in a firm?s weighted average cost of capital (WACC). After all, shareholder value (see Feature, Shares 31 Oct) is best measured by a group?s ability to consistently generate a return on capital employed (ROCE) which exceeds its WACC, so a plan to lower WACC may be helpful.

Cold, hard mathematics show debt is cheaper than equity (see Feature, Shares 24 Oct). A board can therefore manage its charge?s capital structure so the balance sheet is highly ?efficient,? with little cash on it, since this generates a paltry return, a little expensive equity and a lot of cheap debt. Yet the dangers of this are palpable. Investors should therefore make sure the balance sheet can withstand any extra debt that is used to fund any buybacks, while remaining cash and future cashflow must provide enough liquidity for the day-to-day needs of working capital and the payment of bills.

Saddling a company with debt to fund a buyback is rarely a good idea. It increases the risk, so valuation multiples should be lower. Earnings per share, the E in the price/earnings ratio, or PE, may rise on the lower share count, but the price, or the P, should go down, so the share price remains unchanged. Enterprise value (EV) methodologies pick this up, too. The market cap may be smaller, but either cash goes down or debt up to fund the buyback, so the EV does not change.

Executives who think buybacks make their shares look cheaper are therefore kidding themselves and if more debt is to be avoided, so are buybacks which management champions in the name of increased earnings per share (EPS). This is little more than manipulation of the numbers, especially if bonuses are triggered by EPS. In the end, ROCE and cashflow are the real name of the game.

Buybacks also only really work if the stock is cheap relative to its intrinsic value, as estimated by detailed discounted cashflow (DCF) models (see Feature, Shares 16 May). As an investor, the most important determinant of your return is the price you pay and buybacks are therefore no different. If a company?s buyback scheme results in it hoovering up stock at almost any price, rather than only below a set level, it has got the wrong idea. AstraZeneca (AZN) was a sinner on this front until Pascal Soriot canned its buyback programme just over a year ago (see Opinion, Shares 4 Oct ?12).

Income attraction

This leaves dividends. In an era of record-low bond yields and negligible returns on cash in the bank, the income they offer is highly prized by patient portfolio builders, although even these valuable distributions must be kept in perspective. After all, if a company can think of nothing better to do with its cash than give it back to you, then this could mean it is ex-growth. That is likely to impact the rating or valuation multiple afforded to it by the market, as evidenced by utility firms. Alternatively, it may signal management feels the stock is overvalued, as the dividend looks a more sensible option than a share buyback.

A good example of the debate over whether a firm is ex-growth or not is Apple (AAPL:NDQ). Activist investor Carl Icahn is badgering the company to use its massive cashpile to do bigger and bigger share buybacks. At the end of June, the technology giant had $130 billion in cash on its balance sheet and had carried out $18 billion of an authorised $60 billion buyback. Icahn argues the firm should expand its programme to $150 billion, to make its balance sheet more efficient and spice up flagging earnings momentum. Apple?s near-death experience in the 1990s, when it almost went bust, suggests the company will feel more comfortable hoarding its cash, especially as technology firms? earnings streams are not very visible and adding financial gearing to operational gearing is rarely a good idea (see Feature, Shares 7 Nov).

A firm?s growth potential and the valuation of its stock must therefore be considered when you assess a dividend, and your research must also focus on dividend and free cashflow cover to ensure these payments are safe and have the potential to rise (see Cover, Shares Oct 24).

All the quantitative evidence suggests that a growing dividend is a better predictor of share price performance than a high initial yield in isolation. In addition, it is the harvesting and reinvestment of these distributions that mean the stock market has the potential to be a perfect ?get rich slow? scheme. Since its institution in 1962, the FTSE All-Share has advanced at a compound annual rate of 7.1%, albeit with some big swings up and down. In addition, it has paid an average yield of some 3.8%. Had you put £1,000 into the market 51 years ago but banked no dividends it would be worth a tidy £33,057. Had you targeted that 3.8% yield and reinvested it each year in the stocks that paid the dividends, your nest egg would now be £198,848.

Besides the mathematics of dividend reinvestment, increases in these precious payments are a great signal of management confidence in the future. Any board knows it will get grief if the dividend is cut, so any decision to increase the distribution will not be taken lightly.

Investor checklist: when buybacks work

? Highly visible cashflows, themselves a reflection of pricing power and easy-to-forecast volumes, mean the business can easily support any extra debt

? The business does not require major capital investment to remain competitive

? The balance sheet is genuinely inefficient and can take on more debt, subject to the two points above, with the benefit of a reduced weighted average cost of capital (WACC)

? The shares are ?intrinsically? cheap

A strategy case study: Next

Fashion retailer Next (NXT) is perfectly clear about its strategy and its plans are outlined on its website. While Shares has a slight quibble with the focus on earnings per share (EPS), it is hard to argue with the rigorous approach the FTSE 100 firm takes when it comes to achieving its primary financial objective. If every company provided such clarity of vision and transparent disclosure, investors? lives would be so much easier. The Leicester-headquartered concern outlines precisely how it seeks to allocate capital and the clear pecking order it has when it comes to the available options. Note how maintenance and development of product and work on the customer experience - and thus its competitive advantage - are paramount, while sound finances are also put before dividends or buybacks, both of which Next uses to good effect.

Its six-step programme is as follows

? Improving and developing NEXT product ranges, success in which is measured by sales performance.

? Profitably increasing retail selling space. New store appraisals must meet demanding financial criteria before the investment is made and success is measured by achieved sales and profit contribution against appraised targets. The store portfolio is actively managed with openings and closures based on store profitability and cash payback.

? Increasing the number of NEXT Directory customers and their spend, both in the UK and through international online sales.

? Managing gross and net margins through efficient product sourcing, stock management and cost control.

? Maintaining the group?s financial strength through an efficient balance sheet and secure financing structure.

? Generating cash to increase dividends and purchase NEXT shares, when it is earnings enhancing and in the interests of shareholders generally.

This is an edited version of an article that was first published by Shares in November 2013.