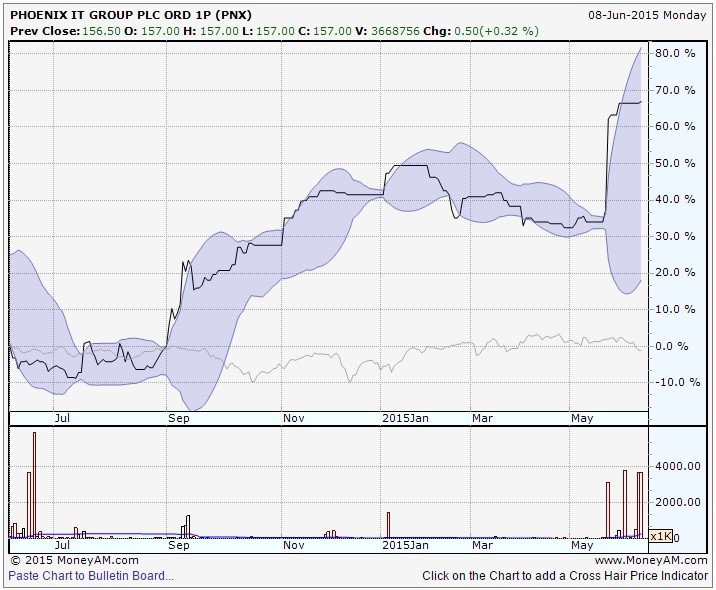

Having arranged today's call with Phoenix IT (PNX) boss Steve Vaughan a couple of weeks back, our conversation would have revolved around the IT services supplier's operational turnaround. But that topic was rendered moot after Daisy's recommended 160p per share, rough £130 million takeover offer 13 days ago (27 May). The stock is at 157p currently.

On that day I raised the question of value, wondering if this was another deal on the cheap orchestrated by Toscafund, the private equity house that owns a little more than 28% of Phoenix stock.

'Remember, it paid just a 9% premium when it took Daisy off the public market, now its offering barely half the value that Phoenix was trading at just five years back. In 2007, Phoenix shares were trading at nearly five quid,' I wrote.

But Vaughan defends the price. He points out that there were contracts in place four or five years ago 'that were on unsustainable margins,' that would never have been repeated. He also says we should bear in mind that some of that business was not real, sparking the company to fess-up to accounting irregularities back in 2012.

The other key point he makes as the company moves from phase one to phase two of its recovery strategy is 'very real execution risk.' Yes, the business has been put on a much firmer footing, substantial progress has been made on net debt reduction (down another £7.1 million last year to March to £49 million) and there is now a go-to-market culture in place that was missing before.

Next comes a focus on cross-selling, margin improvement and new product sales, such as its mid-market CloudSure platform. That won't be easy, far from it. Having consulted all major stakeholders, including many customers as well as shareholders, the decision was in the end an easy one. Customers think combining various IT services with telecommunications leverage is the way forward, management (and most technology followers) agree, and shareholders get a decent premium. Win-win. Shares readers that followed our Play of the Week in April at 126p will net a rough 27%.

Quite how Matthew Riley, Daisy's operational chief, will see the integration and and future of the combined business we simply do not know. But it could be a pretty exciting business if it gets it right, which makes it such a shame that it is no longer on the public market itself. As for Vaughan, he insists that no talks have yet happened about his future, but it seems unlikely that he'll be part of the combined group for very much longer, he wants to run the show, not be a cog in a wheel.