Pharma company Hikma (HIK) continues to have a difficult year after slashing sales forecasts for both its injectables and generics divisions and downgrading full year revenue expectations to $2bn.

This is the second revenue downgrade in 2017, Hikma having guided towards a range of $2bn to $2.1bn in May after its generic version of GlaxoSmithKline’s (GSK) Advair Diskus treatment was delayed.

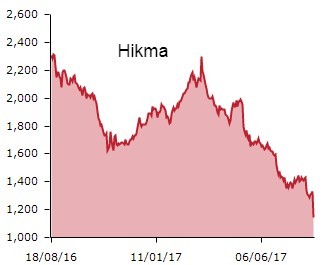

Hikma's shares slide 7.8% to £12.26 with investors alarmed by the company's underwhelming performance and deteriorating outlook throughout 2017 to date.

INCREASED COMPETITION

Hikma expects sales in its injectables division to be approximately $775m in the year to 31 December 2017 as increased competition in the US in the second half of the year starts to bite.

It is a big blow for Hikma as the injectables division represents 40% of overall sales. The company has also flagged lower than anticipated revenue growth in the Middle East and North Africa (MENA) region.

Challenging market conditions in Algeria and the Gulf Cooperation Council, supply disruptions for a key in-licensed product and lower shipments in June were blamed for lower sales. Over the first half of 2017, injectables sales in MENA fell 5% to $35m in constant currency.

The generics division has also been subjected to a sales downgrade of $620m to reflect pressure on prices and volumes.

PRESSURE ON GENERICS

Cantor Fitzgerald’s Brian White says the disappointing performance in generics puts additional pressure on the sterile generics business.

At Numis, Paul Cuddon believes there are bright spots in Hikma’s results thanks to ‘encouraging comments regarding Advair’ and an expanded strategic partnership with Takeda in MENA.

He is confident that Hikma is ‘well placed to trade through the current uncertainty in the US’, flagging 75 product launches so far this year and strong R&D investment to drive a return to strong growth.