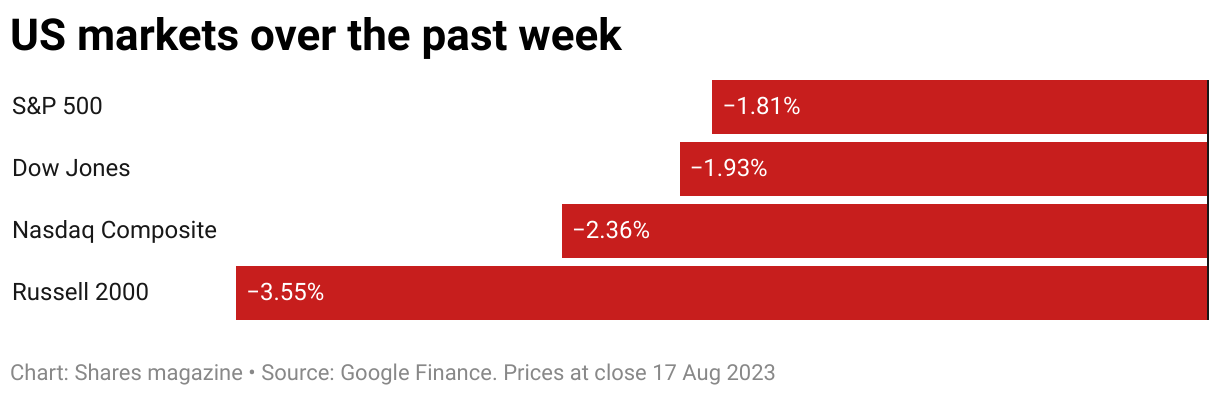

The past week has increasingly taken on a bearish hue on Wall Street as concerns about interest rates and a bubbling Chinese property crisis have begun to dominate.

Minutes of the latest Federal Reserve meeting talking about upside risks to inflation and the need, potentially, for further rate hikes (16 August) helped put upward pressure on US government bond yields and contributed to weakness in stocks.

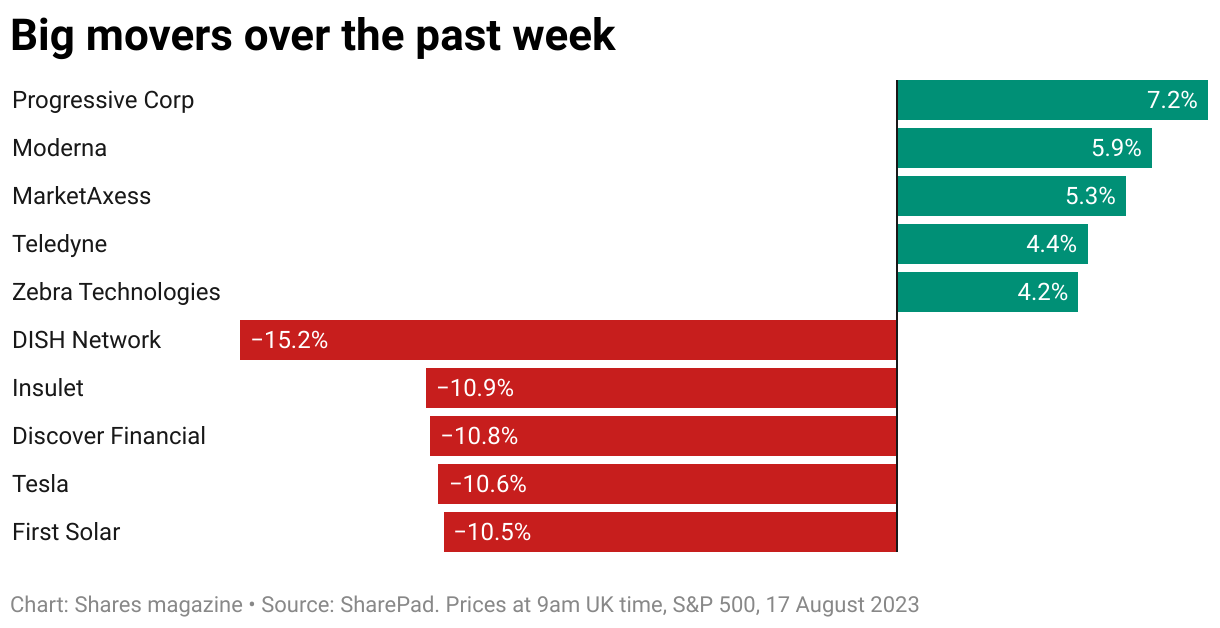

Pharmaceutical firm Moderna (MRNA:NASDAQ) rebounded as it announced one of the key figures in the UK’s response to the pandemic – Jonathan Van-Tam – had agreed to become a medical consultant to the company.

Broadband and TV firm DISH Network (DISH:NASDAQ) was among the top fallers as it filed for an extension with US authorities to come up with the $3.5 billion need to buy 800 MHz licenses from T-Mobile, blaming tough market conditions for its inability to come up with the funds to date.

TESLA

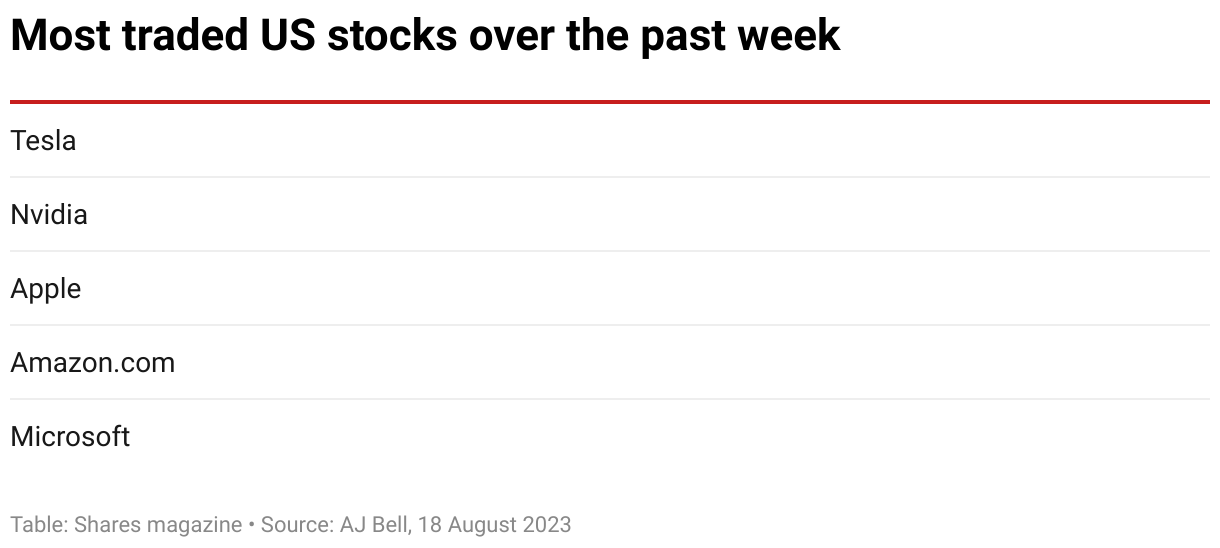

EV (electric vehicle) maker Tesla (TSLA:NASDAQ) was once again the most actively-traded US stock on the AJ Bell platform this week after the firm announced it would cut the price of its cars in China in an attempt to boost flagging sales in one of its key markets.

On Wednesday, the company revealed price cuts across its range, with the Model X reduced to 836,900 yuan ($114,677) against 898,900 yuan previously and the Model S cut to 754,900 yuan ($103,411) against 808,900 yuan, while prices for the Model 3, Model Y Long-Range and Performance editions were also lowered.

Increased competition both at home and abroad has led the company to prioritise volume sales and market share over earnings, with the result that the operating margin fell to 9.6% in the three months to June, its lowest level in five quarters.

Investors are becoming increasingly concerned Tesla may be heading down a one-way street by cutting prices, with the shares losing more than 10% over the last five days to $219.

US-listed shares in Chinese manufacturers such as BYD (BYDBYDBYD:NYSE), Nio (NIO:NYSE) and Xpeng (XPEV:NYSE) also fell on the assumption they would respond with price cuts of their own to protect their share of what is the world’s largest EV market, even though they already have much lower profit margins.

WALMART/HOME DEPOT

Reports of the death of the US consumer have been greatly exaggerated judging by better-than-expected second quarter earnings prints from two American retail powerhouses this week.

Shares in Walmart (WMT:NYSE) ended the week 1.7% weaker at $157.8, despite the retail behemoth raising its full year sales and earnings guidance, having rallied ahead of the results. Walmart’s second quarter earnings per share of $1.84 beat Wall Street estimates as revenues rose 5.7% to $161.6 billion, ahead of the $160.2 billion called for by consensus, as the company’s competitively-priced groceries lured in cash-strapped shoppers.

‘Food is a strength,’ commented chief executive Doug McMillon, ‘but we’re also encouraged by our results in general merchandise versus our expectations when we started the quarter. Our associates helped deliver increases in transaction counts and units sold, and profit is growing faster than sales. We’re in good shape with inventory, and we like our position for the back half of the year.’

Home Depot (HD:NYSE) edged 1.5% higher to $333.4 after it joined Walmart by beating second quarter expectations. The world’s largest home improvement retailer reaffirmed 2023 guidance, and announced a new $15 billion share buyback, after delivering a second quarter comparable sales decrease of 2%, better than the 4.1% drop feared by Wall Street.

Earnings per share of $4.65 were down from $5.05 a year earlier but ahead of the $4.46 analysts were expecting. Home Depot maintained its outlook for the fiscal year 2023, forecasting comparable sales to decline between 2% to 5% for a year-on-year earnings per share reverse of between 7% and 13%.

Chief executive Ted Decker said that while his charge saw strength in categories associated with smaller projects, ‘we did see continued pressure in certain big-ticket, discretionary categories. We remain very positive on the medium-to-long term outlook for home improvement and our ability to grow share in a large and fragmented market.’

CISCO SYSTEMS

Can the tech rally continue through the rest of the year, is one of the big question for investors to answer but noises coming out of Cisco System’s (CSCO:NASDAQ) fourth quarter commentary provided reasons to be cheerful.

Cisco’s networking kit and software effectively provides the nuts and bolts that make the internet work and so it is followed closely as a proxy for corporate spending on technology infrastructure. So far, so good.

Cisco’s Q4 beat estimates on revenues and earnings - $15.2 billion versus $15.06 billion, and $1.14 against $1.06 – thanks to faster inventory run down, but to talk was even better. ‘Cisco commentary was positive on stabilising conditions including that its internal sales forecasts beat in July by several hundred million dollars,’ said KeyBanc Capital Markets analyst Thomas Blakey.

‘The company appeared confident on Ethernet-based AI (Silicon One) opportunities, highlighting $500 million in AI orders to date, but sees demand inflection more likely in full year 2025, similar to peers,’ the analyst added.

Cisco shares jumped around 3% in response to a year high $54.73.