NOT FOR RELEASE, PUBLICATION OR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES, CANADA, JAPAN, AUSTRALIA, OR THE REPUBLIC OF SOUTH AFRICA OR ANY OTHER JURISDICTION WHERE TO DO SO MIGHT CONSTITUTE A VIOLATION OR BREACH OF ANY APPLICABLE LAW.

This announcement is not a prospectus nor an offer of securities for sale in any jurisdiction, including in or into the United States, Canada, Japan, Australia or South Africa.

Neither this announcement, nor anything contained herein, shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction. Investors should not purchase any shares referred to in this announcement except solely on the basis of the information contained in an admission document in its final form (together with any supplementary admission document, if relevant) (the "Admission Document"), including the risk factors set out therein, that may be published by Time to Act plc (the "Company") in due course in connection with a possible offer of ordinary shares in the Company ("Ordinary Shares") and the possible admission to listing of Ordinary Shares to the AQSE Growth Market Access Segment. A copy of any Admission Document published by the Company, will, if published, be available on the Company's website at https://timetoactplc.com/

Embargoed until 7th May 2024

7th May 2024

Time To ACT plc

("Time To ACT", "the Company" or "the Group")

Intention to float on Aquis Stock Exchange Growth Market

Time To ACT plc, an engineering business focused on technology for the energy transition sector, is pleased to announce its intention to seek the admission of its Ordinary Shares to trading on the Aquis Stock Exchange Growth Market (the "AQSE Growth Market").

Highlights

· A UK engineering-led group focused on the Energy Transition supply chain

· Two principal businesses, Diffusion Alloys (coating services, coating technology) and GreenSpur (generator technology)

· Revenue generating and growing topline at ~50% per annum

· Profitable in FY23, with £1.9 million cash in the bank at 31st March 2024

· IP-rich (protected patents, know-how, processes, simulation/modelling and transferable system skills) enabling, what the directors believe to be, first-mover advantages and creating high barriers to entry

· Locally embedded in Middlesbrough, UK (HQ, key management, coatings plant, relationships)

· Experienced Board and Management team

Equity fundraising and WRAP Retail Offer

Given its strong cash position, the Company's application to the AQSE Growth Market is not conditional on it raising funds. However, the Company is seeking to raise up to £1 million of new money to de-risk growth and in support of its strategy of coupling organic growth and acquisition. In addition, it has decided to provide existing and potential new investors with the opportunity to participate in a placing and retail offer via the Winterflood Retail Access Platform (the "WRAP Retail Offer").

The Group is being advised by Novum Securities Limited as its corporate adviser and Oberon Capital as its corporate broker. Retail investors interested in participating in the offer should contact their stockbroker/wealth manager who should contact wrap@winterflood.com.

Commenting on the planned admission and fundraise, Chris Heminway, Executive Chairman of Time To ACT said: "Today marks a pivotal moment for Time To ACT as we embark on the next phase of our journey to address opportunities in the energy transition supply chain. Our decision to float on the AQSE Growth Market underscores our commitment to fostering innovation in this sector and developing engineering-led solutions for a cleaner, greener world.

"It's important to highlight that Time To ACT is well funded and does not require additional capital to list. Nonetheless, we believe that by broadening our investor base, including amongst retail investors, through the Placing and WRAP Retail Offer, we are providing the opportunity for new investors to become part of our exciting journey. I look forward to updating investors on our progress."

For more information, please visit www.timetoactplc.com or contact the following:

| Time To ACT plc

Chris Heminway, Executive Chairman Gary Wallace, Chief Financial Officer |

Tel: +44 (0) 1642 967138 Email: crh@timetoactplc.com Email: gw@timetoactplc.com

|

| Novum Securities Limited, AQSE Corporate Advisor David Coffman, Daniel Harris

| Tel: +4420 7399 9400

|

| Oberon Securities, Corporate Broker Nick Lovering, Adam Pollock, Mike Seabrook | Tel: +44 203 179 5300

|

| St Brides Partners Ltd, Financial PR Ana Ribeiro / Paul Dulieu / Isabelle Morris

| Tel: 020 7236 1177 |

Introduction AND BACKGrouND

The Company was incorporated in England and Wales on 5 July 2011 under the name GreenSpur Renewables Limited and renamed as Time To ACT Limited on 12 October 2019 following the acquisition of Diffusion Alloys Holdings Limited. It converted to a public limited company on 1 November 2023.

The Group is an engineering business focused on technology in the energy transition sector. It currently has two principal operating divisions; Diffusion Alloys and GreenSpur. Time To ACT acts as the holding company for the Group, providing strategic and operational support to the operating companies and capital to enable their growth.

It is the Directors' intention to grow the Group both organically and through the potential acquisition of companies or businesses with complementary technologies in the cleantech sector. Such acquisitions could be of both established and early-stage businesses, as well as intellectual property which would benefit the Group and its strategic aims.

Diffusion Alloys

Diffusion Alloys has been supplying diffusion coating services for over sixty years.

A diffusion coating is an intermetallic layer that protects metal components from degradation at high temperatures and in highly corrosive environments. Diffusion coatings are relatively thin (approximately 25µm-250µm) and diffuse both inwardly into the surface of the base material and outwardly, forming a protective metallic layer at the surface. Formed at high temperatures in a coating chamber, diffusion coatings can provide significant extension of life and remain commercially superior to super-alloys in high temperature environments where corrosion protections helps to determine a system's performance and life expectancy.

Diffusion coatings were first commercialised in the 1950s and initially found only niche applications, prior to an increase in demand for gas turbines (stationary and aero engines) in the period from 1970 to 1990. Diffusion coatings have historically been commonly applied to high-value turbomachinery components (such as gas turbine components) and within the process industry to protect again corrosion mechanisms such as metal dusting and coking.

The Directors believe that Diffusion Alloys is one of only a small handful of companies offering specialist expertise in diffusion coatings as many large competitors appear to offer diffusion coatings only as a sideline to their more mainstream coating services.

During the period 2015 - 2023, Diffusion Alloys undertook a strategic shift which initially involved spinning off the legacy gas turbine business and focusing on clean technology applications. When the legacy business was unable to continue in operation, the former Hatfield site was closed and several key furnaces were relocated to an expanded Middlesbrough site whilst retaining critical diffusion coating expertise for the growing demand from clean technology customers.

Following the site move, the corporate mindset has been revised from being "a coatings plant supported by a technical team" to becoming "a technical coatings capability supported by a plant". This not only changes the manner in which the business approaches its customers but has also enabled the development of an asset-light service offering.

Diffusion Alloys has two revenue streams; coating services and coating technology.

Coating services encompass a range of diffusion coatings aimed at enhancing the properties of the components for improved performance and durability. This service involves plant-heavy work, supplying to volume customers. Services are categorised as either "Large Parts" or "Small Parts", predominantly determined by the size of the components that are coated.

· Large Parts use a gas-powered furnace that can house parts up to 18.5m in length.

· Small Parts use one of several electrically-powered furnaces with a maximum part size of roughly 1.5m in length.

Coating technology focuses on selling the Company's know-how and cultivating early stage revenue opportunities that include compound sales, early-stage coating development work, licensing, equipment sales and laboratory services.

The Directors believe that Diffusion Alloys has three principal selling points:

i) Proven process know-how in the coating of both small and large-scale components;

ii) A dominant market position in the coating of large-scale hydrogen components and comprehensive and advancing references across the emerging Solid Oxide industry; and

iii) A business model offering traditional asset-heavy coating services as well as the sale of asset-light coating technology and the development of a new proprietary diffusion coating process which is intended to materially reduce the capital cost and energy usage of high temperature furnacing.

With its new cleantech-focused approach, the Directors believe that Diffusion Alloys has established a strong international position in the protection of parts against:

i) Catastrophic metal degradation in critical blue hydrogen and other syngas processes;

ii) Severe life-curtailing degradation mechanisms in Solid Oxide fuel cells and electrolysers;

iii) High temperature corrosion and wear from liquid-lead and Lead Bismuth coolants used in both nuclear fission and fusion Gen4 applications.

An important early validation of Diffusion Alloy's cleantech technology and market opportunity was received in the form of a supply-chain partnership agreement with Johnson Matthey plc concluded in February 2023. Johnson Matthey are the market leaders in synthesis gas ("syngas"), a mixture of carbon monoxide (CO) and hydrogen (H2) and have a circa 40% global market share of grey H2 catalysts. As of June 2023, Johnson Matthey had a pipeline of over 35 Blue Hydrogen projects. Under this agreement, the two organisations have joined forces to scale-up production and address the increasing demand for low carbon hydrogen used to reduce global carbon emissions. They will share their complementary areas of expertise and ensure a robust supply chain for the coated components deployed in Johnson Matthey's low carbon (blue) hydrogen offering which enables the production of hydrogen with up to 99% carbon dioxide (CO₂) capture and has already been chosen for several significant projects around the world.

The Directors believe that Diffusion Alloys' value comprises its processes, chemical and metallurgical know-how, which can be seen in its expertise in the coating of small/complex components and in its capacity for large-part coating. It is also developing a new, proprietary diffusion coating process which is intended to materially reduce the capital cost and energy usage of high temperature furnacing.

The Directors believe that Diffusion Alloys' competitive advantages include:

· Proprietary diffusion coatings;

· Experienced technical team working in parallel with customers to develop a solution bespoke to requirements;

· Track record in diffusion coating of small and complex components;

· Rare capability for coating long tubes (in the UK). Expertise in diffusion coating at this scale;

· Re-alignment of company assets to reduce complexity and deploy greater resources to technological and process development;

· Focused research and development ("R&D") projects in place that build on its capabilities for cleantech applications and seek to reduce capital intensity;

· First mover advantage with major competitors seemingly slow to realise the opportunity.

The Directors believe that Diffusion Alloys is the only credible diffusion coater in the world for blue hydrogen components, specifically gas heated/heat exchanger reformers tubes and internal support structures. Within the green hydrogen sector, Diffusion Alloys is already coating in volume for a leading European vendor and is in pre-commercial discussions with a number of other manufacturers.

GreenSpur

GreenSpur is an intellectual property creator and generator designer that has developed a credible solution in renewable energy applications to the Rare Earth magnet problem.1

Magnets constructed using Rare Earth elements (typically Neodymium or Samarium Cobalt) are a fundamental component in electrical generators and electric vehicle ("EV") motors which are critical to delivering the clean energy transition. Yet the world is at risk of not being able to produce or access the electrical power it needs as a result of growing supply chain constraints in the sourcing of Rare Earth elements needed for these magnets. While China controls around 60% of the world market for Rare Earth elements, industry sources claim that it also produces around 90% of the world's Rare Earth magnets. Market concerns about this concentration range from supply/demand imbalances and shortages in the supply volume to the "weaponisation" of Rare Earth elements and Rare Earth magnet supply.

GreenSpur's generator design eliminates the need for Rare Earth magnets and copper coils without any loss in electrical performance, making this technology the conduit between any type of Rare Earth-free magnet and the renewable energy market.

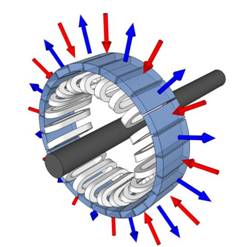

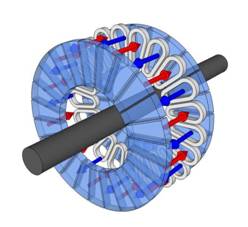

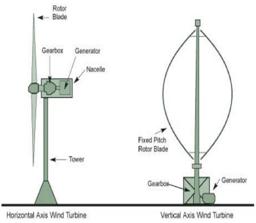

GreenSpur's direct drive generator design is based around an axial flux architecture, as opposed to the more conventional radial flux architecture used in most motors and generators in the wind market. This technology demonstrates a new approach to electrical power generation overcoming historic manufacturing and design issues with axial-flux which some competitors (including wind industry original equipment manufacturers ("OEMs")) have previously been unable to solve.

In conventional radial flux generators, the rotor (rotating part of the generator) and stator (stationary part) are concentric cylinders, with magnetic flux flowing in between them. The flux lines flow to and away from the axis of rotation of the generator along "radial lines". In an axial flux generator, the rotor and stator are arranged as discs along the axis of the machine, and the magnetic flux flows parallel to this axis as "axial lines", as shown in the right-hand diagram below. The advantage of the axial flux topology is that it allows the exploitation of the space envelope and so to increase the quantity of magnets to achieve the desired output.

Arrangement of magnets in radial (left) vs axial (right) flux architecture

The GreenSpur design is modular, with each module containing a rotor, into which the magnets are embedded, sandwiched between two stators into which the coils are placed and in which the current is induced. The design uses ferrite magnets which are widely available and inexpensive, with several advantages over Rare Earth magnets:

· Neodymium Rare Earth magnets can only operate up to 80°C, whilst ferrite magnets can operate up to a maximum 250°C and, therefore, require less cooling infrastructure.

· Ferrite magnets are ~£0.40 per kg, whereas neodymium Rare Earth magnets are ~£50 per kg2.

· Ferrite magnets are more widely available and therefore less susceptible to geopolitical risks

· Ferrite magnet production is more environmentally friendly and can be manufactured from the waste of steel production, whereas Rare Earth elements are mined specifically for magnet production with 1 tonne of Rare Earth elements producing 2000 tonnes of toxic waste.

· Ferrite magnets are more corrosion resistant in wet environments

· Ferrite magnets can withstand higher temperatures than Neodymium Rare Earth magnets

To date GreenSpur has built three prototype generators - a 2kW proof of concept, a 3-stage 75kW demonstrator and a single 250kW stage of a 1MW generator. The Group has 11 patents granted or pending as set out in the table below. It is the combination and linkages of these patents, together with proprietary electro-magnetic and additional modelling, that creates what the Directors believe is a catalyst for the use of Rare Earth-free magnets in wind and renewable energy generation.

The Directors believe that GreenSpur's architecture has three principal selling points:

i) Rare Earth-free and copper-free, thereby alleviating the risk from the supply of Rare Earth magnets being controlled and even weaponised by the largest producers and supply shortages and price spikes of copper (for use in traditional coil windings);

ii) Very versatile as (a) it can be scaled either radially in a single stage or axially with multiple stages as proven with the three prototype generators scaling both axially and radially, and (b) it can be configured to work in any size, any application and with any magnet and any drive train; and

iii) Lowest cost per kW as a result of using inherently cheaper materials than a conventionaldesign - ferrite magnets and aluminium coils as opposed to neodymium magnets and copper coils.

The Directors believe that these key features will position GreenSpur to take advantage of the next-generation (20MW+) mid-speed geared permanent magnet synchronous generators for offshore wind turbines. It is anticipated that the addressable wind turbine market will reach US $129bn by early 2030s. The European Green Deal aims to make Europe climate neutral by 2050. To reach this target, WindEurope calculates that 450GW of offshore wind will be required and that annual installation rates will need to increase from today's 3GW per year to over 20 GW per year in 20303.

It is also increasingly apparent that there is growing concern around there being sufficient supply (and hence the cost) of copper needed to meet the demand for electrical windings. The Directors believe that the Group's aluminium coil design and coil winding capabilities will therefore be increasingly sought after.

GreenSpur's design is suitable for both vertical and horizontal axis designs, with a particular advantage for vertical-access wind turbines (VAWT).

Source: www.centreforenergy.com/

The monetisation model for the Group's intellectual property is through selling design services principally to wind turbine designers but the Directors also intend to sell to other market segments such as new magnet researchers. To date, GreenSpur has secured two initial design services contracts.

The technology is designed initially for application into the multi megaWatt offshore wind industry. As such, GreenSpur's competitors are designers and suppliers of established generator topologies for that market offering radial flux permanent magnet generator technology. Suppliers include wind turbine OEMs as well as outsourced suppliers of motors and generators such as ABB, Flender, CRRC, Weg and others. GreenSpur also competes with other design services businesses such as The Switch or more generalist simulation and modelling companies such as Ansys and Dassault Systemes. This technology is, however, in the Directors' opinion, innovative in the sense that the Directors know of no other businesses attempting to design a Rare Earth-free generator solution or that have successfully overcome manufacturing and design constraints that have prevented the upscaling of axial flux architecture.

Energy Transition

An energy transition (otherwise known as an energy system transformation) is a significant structural change in supply and demand within an energy system. A previous energy transition took place during the industrial revolution and involved a move away from wood and other biomass as fuel to coal and oil, and more recently, natural gas. The energy transition which is currently underway is a transition to clean and renewable energy, driven by the recognition that greenhouse gas emissions must be drastically reduced if the world is to meet its Net Zero commitments and mitigate the process of climate change. This transition involves phasing-down the use of fossil fuels and re-developing whole systems, including transportation and heating, to operate on low carbon electricity.

The Directors believe that the current energy transition will be characterised by three stages:

i) Belief - whether expressed in the form of Net Zero targets, participation in the annual COP conferences or in the growing number of national hydrogen strategies, the world increasingly understands the threat posed by excessive CO2 and methane emissions leading to climate change and global warming;

ii) Financing - funding the new decarbonisation infrastructure, driven by large government wealth funds, hedge funds and private equity funds who are increasingly seeing the opportunity as a new and emerging asset class; and

iii) Supply chain - establishing the supply chain needed to deliver clean technology and renewable solutions by scaling small businesses and establishing new industries to meet the approaching demand.

TTA is positioned in the supply chain stage of the energy transition.

The Hydrogen Market

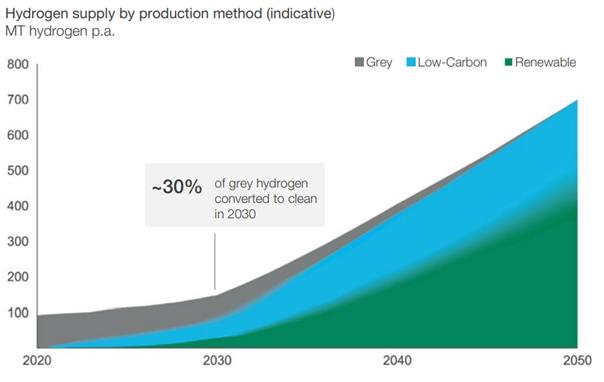

The Directors believe that one of the key features of the Energy Transition will be the emergence of the hydrogen economy. The maturation of the market is now seen as inevitable, even if doubts remain over the timing of market growth.

"Over the last five years, the hydrogen sector has undergone a major maturation. From a niche market, green hydrogen has emerged as a key technology in the journey towards net zero."

Source: ITM Power website (itm-power.com/global-h2-strategies)

"To date, more than 56 countries have released hydrogen roadmaps and strategies."

Source: Centre Of Global Energy Policy (www.energypolicy.columbia.edu/publications/national-hydrogen-strategies-and-roadmap-tracker/)

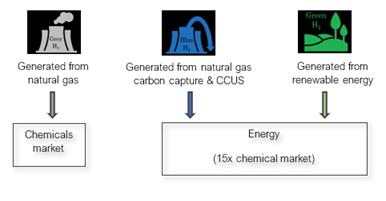

Demand growth for hydrogen will be driven by the expansion of the market from historic applications as, primarily, a chemical feedstock into varying energy applications. The energy market is projected to become 15x the size of the chemicals market (source: Johnson Matthey).

Hydrogen is denominated in various colours referring to its source. In the new hydrogen economy, the market will primarily shift from "grey" hydrogen (produced from steam methane reforming with waste CO2 released to atmosphere) to "blue" hydrogen (produced from methane, but with carbon capture and storage) and then to "green" (generated through the electrolysis of water with renewable energy).

Source: Hydrogen for Net-Zero

Source: Hydrogen for Net-Zero

Future Strategy

The Group's strategy is to operate an engineering development business engaged in advancing multiple subsidiary businesses with relevant technologies that address opportunities within the energy transition supply chain.

TTA's development activity has two discrete elements, comprising:

i) building asset value through intellectual property, patents, know-how, software models, engineering teams, network, processes and vision

ii) monetising the asset value via intelligent business models, revenue streams, solutions selling and strategic partnerships.

The Group operates a centralised financial management model focused on monitoring consolidated development spending, funding sources, cash and cash burn rates and revenues streams. The Group's strategic goal is to ensure that development activity overhead is always funded by a variable combination of commercial revenue streams, external funding and strategic partnerships.

Time To ACT follows six guiding principles:

· Focus on the energy transition sector

· Operate a patient-to-permanent capital model

· Aim to assist operating companies to exceed their potential

· Act as owner / operators

· Have a flexible approach to revenue models

· Work with early-stage to mature businesses

It is the intention of the Directors to consider the acquisition of additional subsidiary companies that fit within this strategy. It is anticipated that any such acquisition would be for a majority stake.

1Intellectual property created by employees/directors of GreenSpur has been transferred to, and is owned by, the Company.

2Commodity prices as at 22 April 2024

3 windeurope.org

4Hydrogen for Net-Zero: Hydrogen Council | McKinsey McKinsey & Company, November 2021

5Hydrogen for Net-Zero: Hydrogen Council | McKinsey McKinsey & Company, November 2021

6The Hydrogen Council and Johnson Matthey plc

7Global Energy Perspective 2023: Hydrogen outlook | McKinsey - www.mckinsey.com/industries/oil-and-gas/our-insights/global-energy-perspective-2023-hydrogen-outlook

RNS may use your IP address to confirm compliance with the terms and conditions, to analyse how you engage with the information contained in this communication, and to share such analysis on an anonymised basis with others as part of our commercial services. For further information about how RNS and the London Stock Exchange use the personal data you provide us, please see our Privacy Policy.