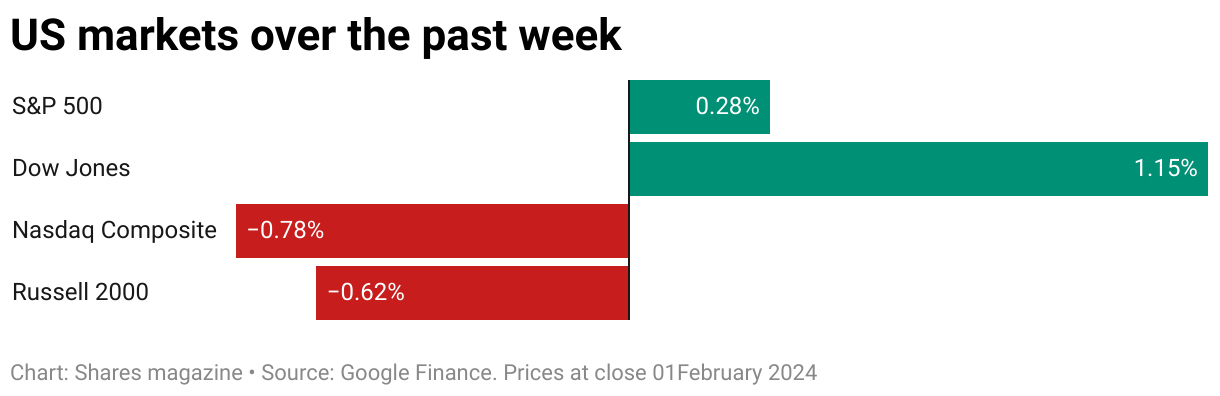

US stocks continued their journey skyward ahead of the Federal Reserve meeting on Wednesday night only to return to earth with a bump on Thursday on a combination of hawkish comments from the central bank and uninspiring tech earnings.

While no-one expected interest rates to be cut from their current level of 5.25% to 5.5%, the monetary policy statement was less conciliatory than expected with Fed chairman Powell reinforcing that view by noting that a March rate cut was ‘unlikely’.

Powell also flagged that long-term inflation expectations are ‘well anchored’ and the labour market remains tight so he is prepared to maintain the current policy rate ‘for longer if needed’.

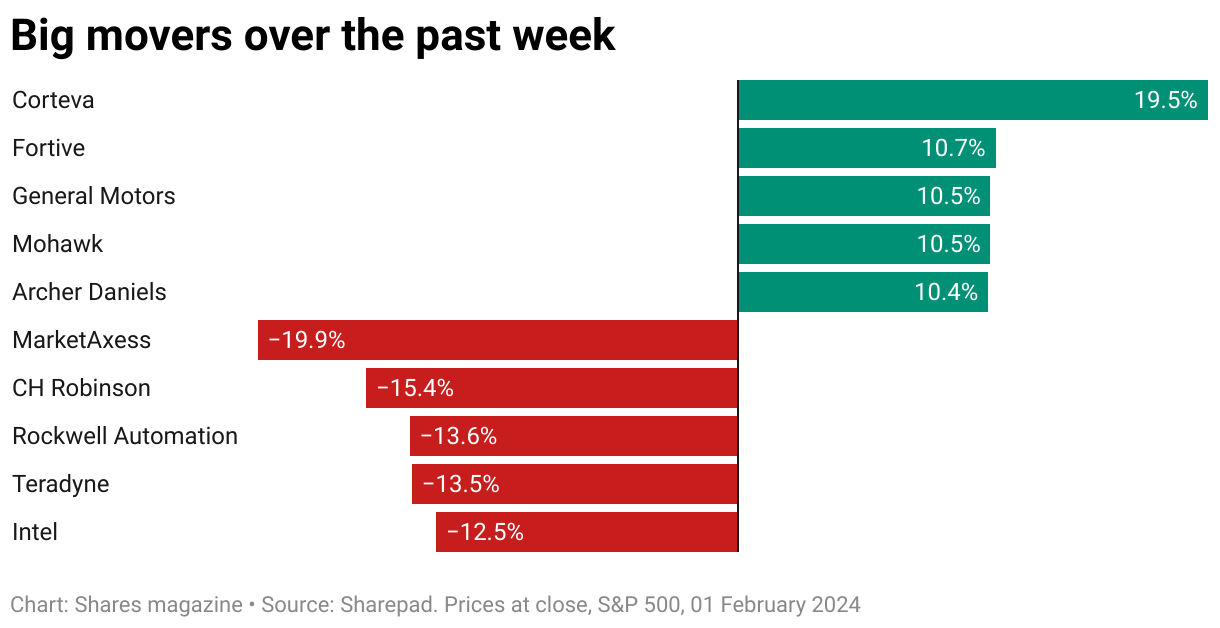

In terms of tech earnings, Amazon.com (AMZN:NASDAQ) and Meta Platforms (META:NASDAQ) pleased investors, with the latter's shares jumping 14% to a record high and the two firms adding more than $280 billion to their market caps, but it was a less happy story at Alphabet (GOOG:NASDAQ) and Intel (INTC:NASDAQ).

ALPHABET

‘Could do better’ was the general sentiment towards Google-owner Alphabet (GOOG:NASDAQ) as its fourth-quarter earnings fell short of expectations. Alphabet shares have lost 5% or around half of their year-to-date gains over the past few days.

So, what has gone wrong for one of the ‘Magnificent Seven’? On the face of it, 13% growth in consolidated revenues to $86 billion is respectable, while Google Cloud revenue and YouTube ad sales were in line with Wall Street estimates at £9.2 billion helped by the NFL package, but in reality, Alphabet is being trounced by the competition and investors know it.

The impact of generative AI on search, plus Microsoft’s (MSFT:NASDAQ) tie up with startup Open AI, are all possible threats to Google-owner Alphabet. Investors need some reassurance that everything the company is spending on AI will pay off in the future and enhance its advertising offering.

MONDELEZ

Known for iconic brands including Oreo, Cadbury Dairy Milk, Toblerone and Ritz, snacking behemoth Mondelez (MDLZ:NASDAQ) cooked-up forecast-beating sales and EPS (earnings per share) for the fourth quarter to 31 December 2023.

However, the share price soured on results day (30 January) as investors digested a 0.4% decline in volumes and weak guidance for 2024 from the Chicago-based consumer staple.

Mondelez reported better-than-expected quarterly EPS of $0.84, up 23.5% year-on-year, as sales fattened up 7.1% to more than $9.3 billion, yet a 5.5% decline in North America volumes suggested price hikes are beginning to catch up with Mondelez and light 2024 guidance also left investors with a bad taste.

Dirk Van de Put-led Mondelez now expects organic net sales growth for 2024 at the upper end of the 3% to 5% range, a sharp slowdown from last year’s 14.7% growth rate blamed on ‘greater than usual volatility as a result of geopolitical uncertainty’. A post-results rebound left Mondelez shares up 1.1% for the week at $75.5.

MICROSOFT

A spot of profit taking was always possible on Microsoft’s (MSFT:NASDAQ) latest earnings release. A near 10% rise in January, breezing beyond the $400 mark for the first time ever (even adjusted for past stock splits), means the share price has rallied nearly 25% since the end of October 2023, building on a 50%-plus rally over the past year.

It is now the world’s largest company, overtaking Apple (AAPL:NASDAQ), no mean feat.

Clearly, an awful lot of progress was already built into consensus, so when numbers came in impressively above that mark, that they were not ‘blow out’ led to a not unreasonable pause. They say it is never wrong to take a profit, and while there are plenty that would argue the point, it is a widely enough followed investment principle to comprehend a little stake top-slicing.

‘The key highlight is the 20% growth of Intelligent Cloud, reaching $25.9 billion, fuelled by a 30% (28% at constant currency) increase in Azure and other cloud services’, said Megabuyte analyst Ieuan Turner.

The Q2 launch of Copilot propelled Azure AI customers to around 53,000, a significant increase from 18,000 in September and 11,000 in July.

Q3 revenue guidance is for around 10% to 12% on the Productivity and Business Processes side, 11% to 14% for Personal Computing, but Intelligent Cloud will again lead the way, where 18% to 19% growth implies $26 billion to $26.3 billion of sales.