Wall Street closed out August in decent fashion, although some of the momentum was taken out of the recent rally by a mixed reading on US inflation.

The Core PCE index – closely followed by the Federal Reserve when making interest rate decisions – was roughly in line with forecasts but, nonetheless, showed a slight tick higher year-on-year.

August as a whole represented the first monthly back step for US markets since February as concern about inflation and worries relating to the Chinese economy conspired to trip up stocks.

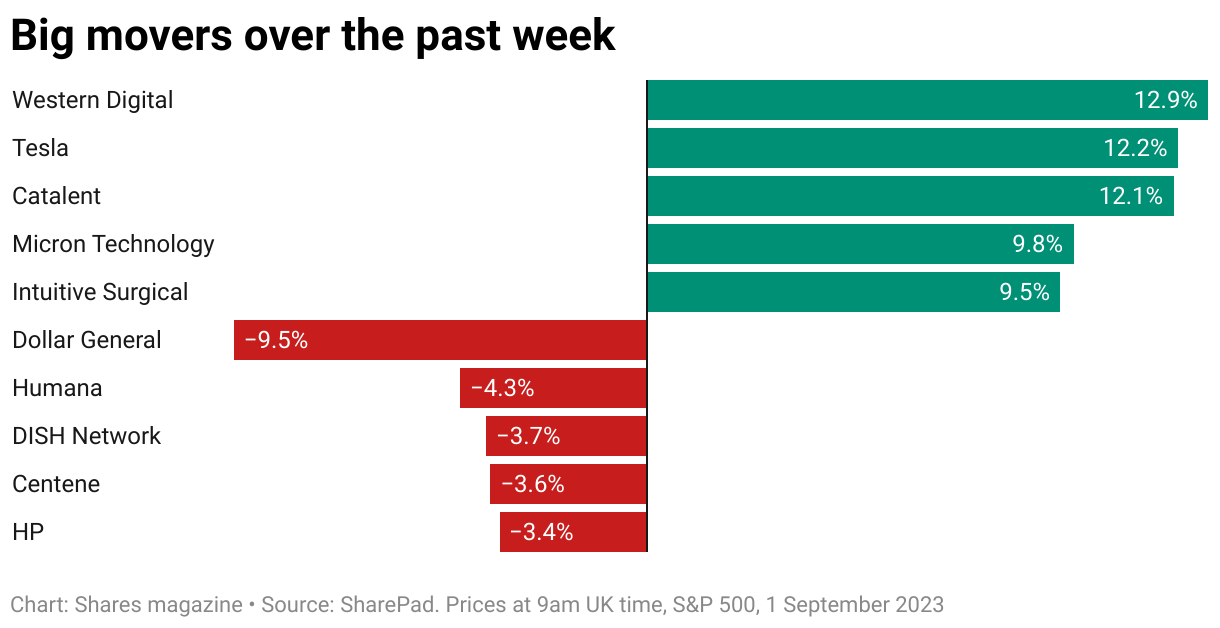

Electric vehicles leader Tesla (TSLA:NASDAQ) enjoyed a strong week as it unveiled a refresh of its popular Model 3 sedan and announced further price cuts to boost sales in the US and China. Positive commentary from Morgan Stanley helped give a lift to San Jose computer drive manufacturer Western Digital (WDC:NASDAQ).

On the flipside, health insurer Humana (HUM:NYSE) saw its shares come under pressure and TV provider DISH Network (DISH:NASDAQ) continued to struggle, extending its losses over the past month to more than 20%.

ELF BEAUTY

Boasting one of the more attractive share price charts on Wall Street, mass-market cosmetics brand Elf Beauty (ELF:NYSE) powered 14% higher to $136.9 after investors applauded its $355 million acquisition of skincare disruptor Naturium (29 Aug).

The cash and shares deal is expected to double Elf’s skincare sales, boosted by direct-to-consumer distribution via Amazon’s global platform and partnerships with Target (US) and SpaceNK (UK). Elf, or eyes, lips and face, if you were wondering, continues to gain market share, offering what it believes are premium quality cosmetics at affordable prices, largely to 20, 30-somethings.

In August, Elf raised its fiscal 2024 outlook after posting quarterly net sales growth of 76%, marking 18 consecutive quarters of average sales growth above 20%. Wall Street evidently loves the story, with shares in Elf Beauty up more than 260% over the past year, even better than AI chips darling Nvidia (NVDA:NASDAQ).

DOLLAR GENERAL

Shares in discount retailer Dollar General (DG:NYSE), one of America’s most successful chain stores, fell 16% to $131 after it reported second-quarter earnings which missed expectations and lowered its guidance for the full year.

Earnings per share of $2.13 were well short of consensus estimates of $2.47, while net revenue of $9.8 billion also missed forecasts which were pegged at $9.93 billion. The firm blamed declining footfall and lower like-for-like sales in home, seasonal and clothing, which was only partly offset by consumables.

Gross profit declined due to ‘lower inventory markups and increased shrink, markdowns, and inventory damages, as well as a greater proportion of sales coming from the consumables category, which generally has a lower gross profit rate than other product categories,’ the firm said.

The mention of shrink – or theft from its stores – echoed comments made last week by Dick’s Sporting Goods (DKS:NYSE), whose chief executive admitted he had underestimated the impact ‘organised retail crime’ would have on its sales.

Dollar General also lowered its full-year same-store sales growth target and its profit guidance, with earnings per share now seen in the range of $7.10 to $8.30, a decline of between 22% and 34% against an 8% decline forecast previously.

OKTA/CROWDSTRIKE

As we’ve seen from recent comments around Darktrace (DARK) and Palo Alto (PANW:NASDAQ), demand for cybersecurity solutions remains robust. It’s a trend that saw shares in US-listed Okta (OKTA:NASDAQ) and CrowdStrike (CRWD:NASDAQ) to rally over the past week after both companies reported better-than-expected earnings and revenue in their most recent quarters.

CrowdStrike’s strong figures were driven by customer growth, with annual recurring revenue up 37% year-on-year to $2.93 billion as of end July, while subscriptions gross margins came in at 80%, up from 78% the year prior. Okta’s subscription revenue in the quarter came in at $542 million, up 24% year-on-year, its remaining performance obligations, or subscription backlog, was $3.03 billion as of the end of the quarter, up 8% year-on-year, sparking a 10% after-hours share price pop.

Encouragingly, both companies are also sitting on hefty cash piles of $3.17 billion and $2.11 billion respectively, leaving plenty of firepower for future investment and possible acquisitions.