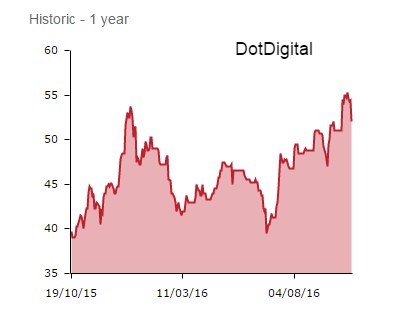

Shares in the software supplier to the digital marketing industry have dropped more than 4% to 52p on Tuesday. That's a seemingly weird response to full year results (to 30 June) showing revenues up 26% to £26.9m and adjusted EBITDA up 17% to £8m. For the record, pre-tax profit at a fraction more than £6.2m implies an 18.5% increase year-on-year.

You can't even criticise DotDigital's (DOTD:AIM) cash generation, an area where many software companies fall down. Cash generation is strong and getting better, recording an £8m cash inflow from operations, funding net tax and interest charges of £0.3m, capex of £2m and dividend of £1.1m. After £0.8m of share issue proceeds DotDigital ended the year with a £17.3m debt free cash pile, up from £11.9m at the end of fiscal 2015.

DotDigital provides SaaS (software as a service) solutions and managed services to digital marketing professionals. The company’s core SaaS technology, dotmailer, provides marketers with a single solution to engage customers through email, mobile, social media and landing pages. The solution can be integrated with CRM, e-commerce and other third-party applications.

One area of perceived weakness is in the US. Even the company itself reckons it's been a slow start despite revenues jumping 43%, from $3m to $4.4m, or £3.6m from £2.45m in pounds, for consistencies sake. Now with a New York office that will act as a hub across the States, new staff hires, and a strengthened partner network, the US has the potential to put up big growth numbers down the line.

The other potential sticking point for investors is the shares' already beefy rating. Based on the 54.38p share price pre today's results the implied PE rating for June 2018 was around 20, so a fair bit of excitement is already in the price.

But we can think of many technology companies trading at far heftier ratings than this, many of them without the growth profile, cash generation or dividends of DotDigital. By the way, there's also a full year 0.43p per share ordinary payout topped up with a 0.41p special dividend. Sure that's just a 1.6% yield, but this is a genuine growth stock.

Small cap fund manager Philip Rodrigs, of River & Mercantile, is a long-run fan, which you can read about here.