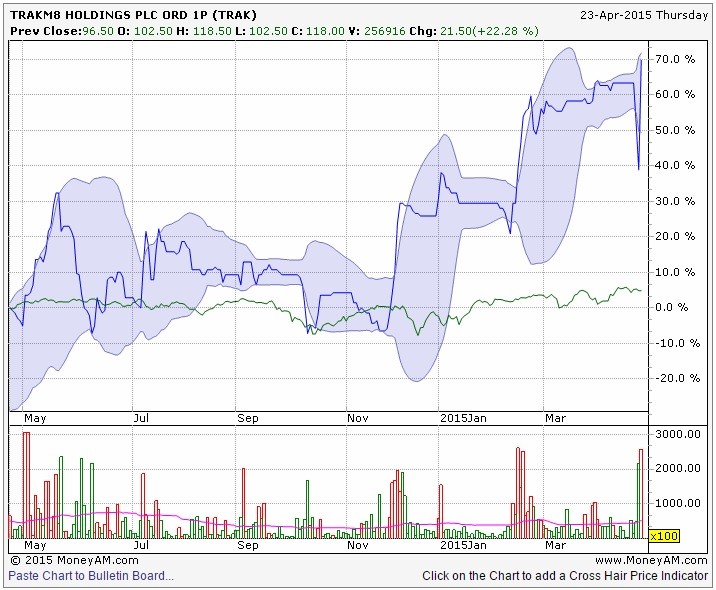

When management of small cap companies get this excited about their company's prospects it's sometimes a signal for investors to be wary. AIM-listed vehicle telematics supplier Trakm8 (TRAK:AIM) announced today an astonishing 95% hike to full year revenues for the year to end March, 73% of which is organic (approx £6.4 million), with the remainder coming from BOX Telematics, acquired in October 2013.

Yet this is not really the reason why the shares jumped 22% today to 118p. The market was already anticipating such a sales jump, with forecasts pitched at £18 million, up from £9.2 million the year before, funnily enough, a 95% rise (or 96% if we round up the figure). Earnings before interest, tax, depreciation and amortisation (EBITDA) of £2.4 million was pencilled in, for a 13% margin.

So what's getting investors excited? Two things, as far as I can see. Firstly, management have also said this year's (to March 2016) guidance is too low.

'Revenue for the new financial year ending 31 March 2016 is now expected to be ahead of previous management expectations, with profits comfortably ahead of previous management expectations,' the company says.

According to FinnCap's estimates*, the house broker, EBITDA of £3.1 million on £21.3 million revenue had been expected, implying 8p per share of earnings. So scratch that, we're maybe looking at a 20% beat on that EPS figure, implying 9.6p, which suddenly slashes the current year price to earnings (PE) multiple from just below 15 to just over 12, and that's after today's shares surge.

The other point is how it makes its money. Supplying the hardware, yes, but that's relatively low margin stuff. It's the data those boxes send back to Trakm8's servers that's more interesting, which gets supplied to motor insurance customers so they can analyse driving habits and price policies accordingly. That's especially important for younger and inexperienced drivers, such as the 17-25 year old's that car and insurance supplier Marmalade specialises in. It signed a £1 million contract with Trakm8 in February, and other deals are being struck too.

This is reflected in stated annualised recurring revenues up 60% for last year to £7.3 million, or a little over 40% of the company total, a fast-growing and presumably reliable future income stream.

*FinnCap's new estimates are for £22.5 million revenue, and £3.4 million EBITDA, which works out at 9.1p EPS and implies a PE of 12.9. But we'd expect analyst Lorne Daniel to factor in a little caution, it never hurts to under-promise and over-achieve.