- Global dividends down 0.9% in Q3

- Biggest cuts from mining sector

- Banks contributed most to growth

Steep cuts from a handful of companies meant that global dividends fell slightly in the third quarter of 2023, according to the latest Global Dividend Index from Janus Henderson.

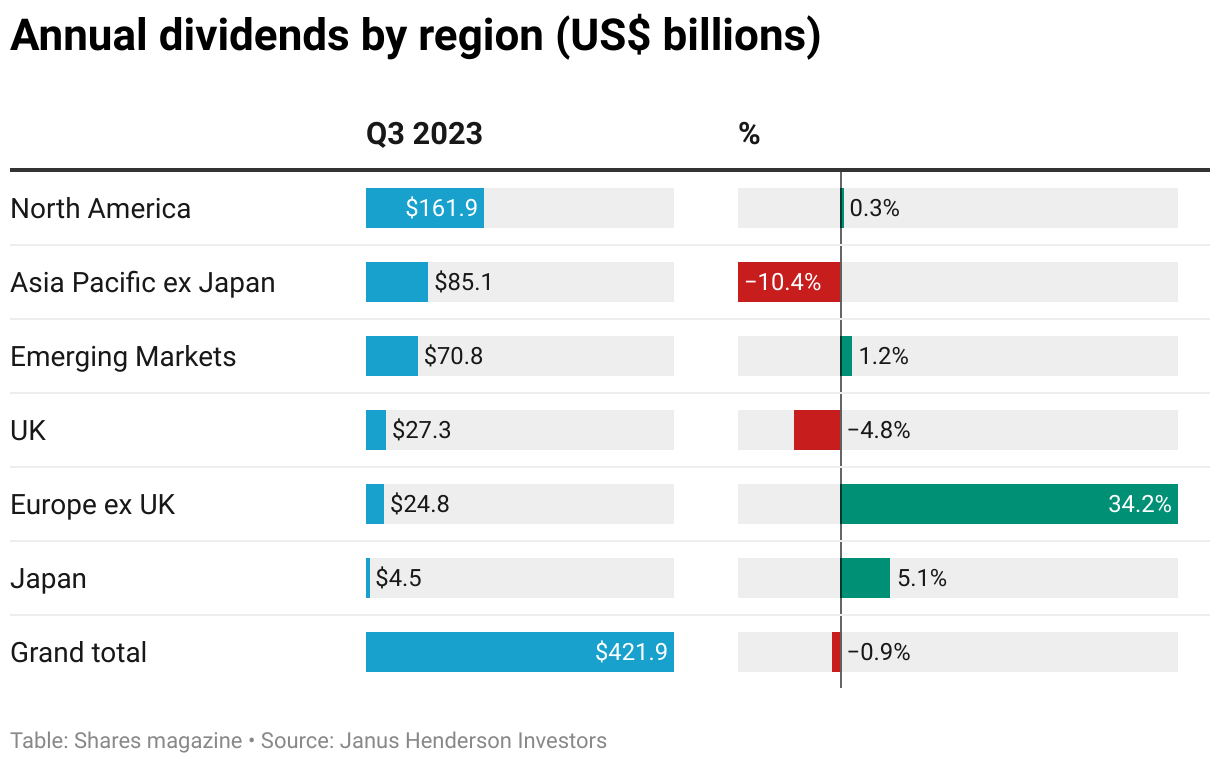

The asset manager’s latest study, which tracks dividends paid by the largest 1,200 companies around the globe, revealed third quarter dividend payouts slipped 0.9% globally to US$421.9 billion.

However, underlying growth was 0.3% after adjusting for lower special dividends and the strengthening US dollar, while Janus Henderson stressed that large cuts from a few big companies ‘masked much more promising growth around the world’.

And while the asset manager has slightly trimmed its headline global forecast for 2023 payouts from $1.64 trillion to $1.63 trillion, headline global dividend growth is still forecast to be a healthy 4.4% year-on-year.

LOFTHOUSE LOOKS AHEAD

Ben Lofthouse, head of global equity income at Janus Henderson, explained the apparent weakness in Q3 global dividends is ‘not a cause for concern, given the large impact a handful of companies made. In fact, the level and quality of growth look better this year than seemed likely a few months ago as payouts have become less reliant on one-off special dividends and volatile exchange rates.’

Underlying dividend growth was 5.3% if the two largest cutters were excluded, while 89% of companies in the index either raised dividends or held them steady.

QUARTERLY CUTS

In the quarter, the biggest cuts emanated from the mining sector, where half of companies reduced payouts, and from oil producers in Brazil and Taiwan.

The two biggest cuts came from Brazil’s Petrobras (PBR:BCBA) and Australian miner BHP (BHP) – their impact was so large that removing them revealed 5.3% global underlying growth in Q3, in line with the longer-term trend.

Dividends from chemicals and Asian real estate companies were also down sharply amid challenging economic conditions in the region.

BANKS RIDE TO THE RESCUE

Dividend cuts were offset by strong banking dividends in most parts of the world, with banks contributing most to growth in Q3, adding $5.8 billion or 9.3% year-on-year, as well as by rising payouts across sectors including utilities and vehicle manufacturers.

In terms of geographic regions, growth from banks, oil producers and utilities offset mining sector cuts in the UK, while Europe continued to exhibit very strong growth with payouts across the region powering 22.9% higher on an underlying basis, leaving Europe comfortably on track to deliver record distributions this year.

Chinese dividends reached a new record thanks to a large increase from Petrochina (0857:HKG), but this masked weakness among Chinese banks and property companies.

Janus Henderson also highlighted ‘slow yet robust growth’ in the US, where dividends grew at 4.5%, ‘a healthy rate of growth albeit slower than preceding periods’ with 98% of US companies either raising payouts or holding them steady.

However, the US was outpaced by Canada, which is benefiting from strength in the banking and oil sectors.

Janus Henderson’s Lofthouse added: ‘Dividend growth from companies generally remains strong across a wide range of sectors and regions, with the exception of commodity-related sectors, such as mining and chemicals. It is quite common and well-understood by investors that commodity dividends will rise and fall with the cycle, however, so this weakness does not suggest wider malaise. Moreover, our figures show that a globally diversified income portfolio has natural stabilisers – sectors in the ascendance, such as banking and oil, have been able to counteract those with declining dividends.’