Science and technology kit designer SDI (SDI:AIM) will crush pre-existing financial performance forecasts this year and next after securing ‘material’ follow-on orders for its Atik cameras business.

The order comes from a major original equipment manufacturer (OEM) of real-time PCR DNA amplifiers, after an initial contract won by SDI in 2020.

Delivery timing of orders remains up in the air but the company believes that it will ‘exceed the market’s sales and profit expectations’ this year to 30 April 2021 and ‘substantially exceed’ next year’s numbers.

This is despite SDIO admitting that most of its businesses had seen revenue negatively impacted by the Covid-19 pandemic.

BLOWN OUT OF THE WATER

Analysts at FinnCap had been anticipating roughly £5 million of pre-tax profit on £28 million to £29 million revenues but has now ripped up those estimates.

The broker’s new forecasts are pitched at £6.7 million and £8.8 million pre-tax profit on £34 million and £42.1 million sales for this year and next respectively.

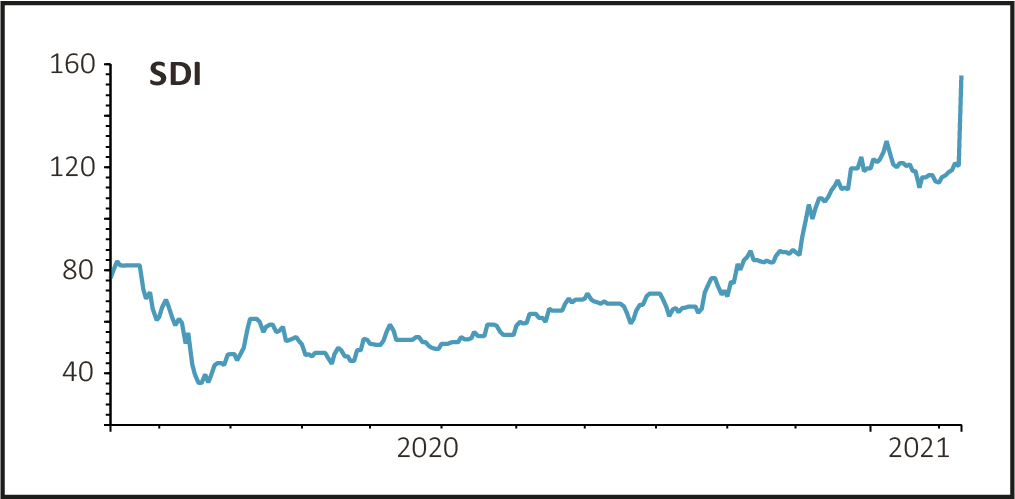

The news saw SDI stock soar 27%, setting a new all-time record of 153p and valuing the AIM-quoted business at more than £150 million.

SDI is a collection of multiple subsidiaries that design and manufacture digital imaging, sensing and control equipment used in life sciences, healthcare, astronomy, manufacturing, precision optics and art conservation applications.

It is a model that closely resembles that of health, safety and environmental kit maker Halma (HLMA), a constituent of the FTSE 100.

FIRM FAVOURITE WITH ORDINARY INVESTORS

SDI has built a loyal retail investor fanbase over the years, much like Judges Scientific (JDG:AIM), the £410 million that pursues a comparable acquisition-led strategy in the science and technology field.

FinnCap upped its target price for the shares from 130p to 180p, which would imply the stock trading on full year April 2022 enterprise value (EV) to sales of 4.1-times, the broker calculates. A 180p share price would also imply a 16.6-times EV/EBITDA (earnings before interest, tax, depreciation and amortisation) and adjusted price to earnings (PE) multiple of 25.3, underpinned by circa 60% earnings per share (EPS) growth in full year 2021 and 28% in 2022.

‘This would imply a circa 4.3% free cashflow yield, offering scope for further appreciation given that its more mature peers (Judges Scientific and Halma) trade on circa 21-times EV/EBITDA with prospective free cashflow yields of 2.1% to 2.5%’, said FinnCap’s Mark Brewer.